If You’re Still Thinking About Retirement Like Your Parents Did, Read This

Change is all around us and can occur slowly over time, like a river carving through rock until a canyon forms, or it can happen as quickly as a lightning strike. Retirement has evolved significantly and will likely continue to change throughout your lifetime, even more so for your grandchildren. In this discussion, we will explore some of the major changes that retirement and retirement planning have undergone. Additionally, we’ll discuss how you can adjust your mindset to embrace a modern approach to retiring.

Key Points – If You’re Still Thinking About Retirement Like Your Parents Did, Read This

- A Shift in Retirement Responsibility:

- Increased Life Expectancy:

- Increased Retirement Age:

- Inflation:

- Conclusion:

- Schedule a Visit

A Shift in Retirement Responsibility:

Your parents or grandparents may have had pensions, which are employer-sponsored retirement plans that provide regular payments during retirement. While some government jobs still offer pensions, most employees are now required to take more responsibility for their retirement savings by using 401(k) plans or IRAs.

401(k) plans offer more flexibility and come with the potential for higher risk and growth, but they also require individuals to manage their investments actively. As the job market has evolved, with fewer people staying at the same job for many years, this flexibility has become increasingly important in navigating the changing landscape of employment.

Increased Life Expectancy:

With medical advancements, people are living longer, which leads to longer retirements that need to be financed. Healthcare advancements have significantly contributed to increased life expectancy, but they have also led to rising costs. According to U.S. News, healthcare expenses have surged by over 121% since 2000, even with Medicare coverage.

Living longer is a blessing, as it allows us to witness the growth of our families and the thriving communities we help build. It’s important to be fully engaged in these moments rather than constantly worrying about finances or whether you’ll outlive your retirement savings.

To prepare for those extra years of retirement, it’s essential to consider make a financial plan and understand the risks. Be cautious of the sequence of returns risk, which refers to the potential for poor investment returns occurring early in retirement. When you withdraw from your portfolio during these times, it can damage your investments and leave you vulnerable to running out of money. Timing is crucial in mitigating this risk and ensuring your financial stability throughout a longer retirement.

Learn More: Sequence of Returns Explained (And Why It Matters Most Near Retirement)

https://www.youtube.com/watch?v=5hzWnueMiCQ&t=2s

Increased Retirement Age:

The concept of retirement is evolving; it's no longer just a standard age of 65. Many retirees are choosing to continue working during their retirement years, and there are discussions about potentially increasing the retirement age again.

According to Senior Living data from 2010 to 2019, participation in the labor force among adults aged 65 and older rose from 17.4% to 20.2%. This increase may reflect a desire to stay active or busy, as many older adults feel the need to work. Additionally, the poverty rate among older adults has significantly declined, from 30% in 1966 to 10% today. Improved financial education has played a key role in this reduction.

However, despite the decline in poverty, there are ongoing concerns regarding healthcare costs, rising obesity rates, and chronic conditions. Moreover, issues such as divorce contribute to feelings of loneliness and isolation among retirees.

Learn More: Planning For the Medical Costs You Don’t See Coming in Retirement

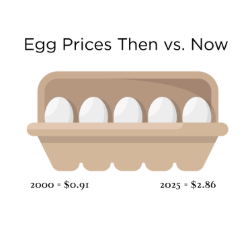

Inflation:

Inflation continues to change our perception of money and what a dollar can actually buy. Additionally, older generations have influenced our views on money and retirement. While the impact of inflation is noticeable when purchasing groceries, the more concerning issue is its long-term effects. A 3% annual increase may not seem significant, but it’s important to remember that retirees are living longer than ever, and inflation is a constant factor. It is essential to develop a plan that will help maintain your purchasing power so you can sustain your lifestyle for as long as needed, without financial worry.

Learn More: Are You Aware of Inflation and Its Impact on Your Retirement

Conclusion:

Retirement is set to evolve significantly in the coming years, even more so than it has in the past. What is true for you now may not be the same for your children or grandchildren. Change is a natural part of life and occurs all the time. You can navigate the world of retirement with confidence, and it all begins with a solid plan and the knowledge to help you continue enjoying retirement for many years to come.

GET IN TOUCH

Schedule a Visit

Past performance is not indicative of future results. The material above has been provided for informational purposes only and is not intended as legal or investment advice or a recommendation of any particular security or strategy. The investment strategy and themes discussed herein may be unsuitable for investors depending on their specific investment objectives and financial situation. Information obtained from third-party sources is believed to be reliable though its accuracy is not guaranteed, and 210 Wealth Management, Inc., d/b/a 210 Financial makes no representation or warranty as to the accuracy or completeness of the information, which should not be used as the basis of any investment decision. Information contained on third party websites that 210 Financial may link to are not reviewed in their entirety for accuracy and 210 Financial assumes no liability for the information contained on these websites. Opinions expressed in this commentary reflect subjective judgments of the author based on conditions at the time of writing and are subject to change without notice. No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission from 210 Financial. For more information about 210 Wealth Management, Inc., d/b/a 210 Financial, including our Form ADV brochures, please visit https://adviserinfo.sec.gov or contact us at (309)263-1333.