The 210 Financial Blog

Your Source for REtirement Insights

Your Thought Partner in Retirement

Financial planning can feel complex, but staying informed about it shouldn’t be. The “210 Financial Blog” offers timely articles, practical thinking and clear information to help you navigate the money world.

The 210 Financial Blog

Retirement Planning for Married Couples

Remember the vows you took at your wedding, pledging your commitment to one another through good times and bad, in sickness and in health, for richer or poorer, until death do you part? Those heartfelt promises mark a special time in your lives—a joyful celebration filled with love. You committed to loving one another through every challenge, even as you look forward to a blissful retirement together.

By choosing to prioritize your partnership and work towards building a shared life, you create something truly beautiful. Now you are ready to build your next chapter together: retirement. We’re here to guide you with helpful retirement planning tips specifically for married couples.

Key Points – Retirement Planning for Married Couples

- Starting Your Retirement Plan with Income Planning:

- Finding Affordable Life Insurance:

- Finding Affordable Healthcare in Retirement:

- Investment Planning Mindset Shift in Retirement:

- Financial Advisor Specifically for Retirement:

- Legacy Planning for You and Your Spouse:

- Conclusion:

Starting Your Retirement Plan with Income Planning:

When you plan your wedding, it is filled with planning down to even the smallest detail. Planning your retirement together is no different. There are small details and big obstacles that you have to decide and plan for your life together. Entering retirement together comes with its unique set of challenges and rules.

So start with a plan that can help you and your spouse thrive in retirement. A plan helps you know where you are and where you need to go and what to do to achieve your retirement dreams.

When you build anything, you need a solid foundation and retirement that starts with your income and building a plan that ensures you both get a paycheck for the rest of your lives.

That’s where an income plan comes in handy, to give you a solid foundation and make sure that even without a paycheck, you can still pay yourself. The largest issue with income planning is how long people are living. Thanks to advances in healthcare, people are living longer, meaning retirement is now longer than it has been in the past. And you need money to cover living longer and to do all the things you dreamed about for your retirement together.

How much money is enough to cover a longer retirement? Focusing on one singular number isn’t the right way to approach this question. Talking with a financial advisor can help you better understand where your plan is and where it needs to go.

Staring with your sources of income:

- Social Security – since your first paycheck you’ve been contributing retirement is when you get to cash in on that promise. Social Security benefits, and what your are eligible to receive. To get a clear picture of your estimated benefits, visit www.ssa.gov/myaccount.

- To qualify for spousal benefits with Social Security, you must be married to someone who has worked and is currently receiving benefits. Additionally, the non-working spouse must be at least 62 years old. While spousal benefits generally mirror the standard benefits, there are a few key exceptions to note:

- Growth Limitations: Spousal benefits stop increasing once the non-working spouse reaches full retirement age, at which point they receive 50% of the working spouse’s benefit.

- Survivor Benefits: Your spouse may be able to claim your benefits if you die.

- Divorced Couples: Even divorced individuals can qualify for spousal benefits, provided certain conditions are met.

- Pension – if you have one like most government jobs have

- 401(k) and IRA – your retirement accounts in retirement when you start to pull money out of them they will help you pay yourself.

- Other:

- Life Insurance

- Annuities

- Long-term care insurance

- Stock & bond portfolios

- Liquid assets (what is in your bank account)

- Rental properties

Sit down with your spouse and review all your income sources, both big and small, to better understand what you will have coming in during retirement.

Learn More: Why Many Retirement Plans Fail

https://www.youtube.com/watch?v=B20JiNuxHgc

Finding Affordable Life Insurance:

Life insurance is often misunderstood; it's not for you, but for your loved ones and your spouse. If you haven't thought about it before, now is the time to consider it for their sake. There are many options available, so be sure to research and find the one that is right for you.

A survey conducted by the Life Insurance Marketing and Research Association revealed that individuals aged 25 to 40 often overestimate the cost of life insurance, believing it to be three times more expensive.

You are neither too young nor too old to obtain a life insurance policy. Starting young typically means lower premiums and can also provide protection for parents or co-signers. For individuals over 60, life insurance premiums tend to be higher due to an increased risk of age-related health issues. However, if you have individuals who depend on you financially, it’s essential not to overlook this option, even with the higher costs.

Finding the policy that is best for your family or spouse is the most important part, people rely on you to help cover finances and find something to ease their burden. A good place to start is to investigate both whole life insurance and term life insurance and which one makes more sense for you. They both offer a death benefit to the beneficiaries. The main difference is that whole life insurance offers the death benefit for the entire lifetime and term life insurance is only within a certain time frame.

- Burial insurance is a whole-life policy to cover your future burial and other end-of-life expenses.

- Survivorship life insurance a type of joint policy that covers two people instead of one, offering the same characteristics and benefits as individual life insurance.

- Universal life insurance is a type of whole life insurance that offers lifetime coverage and builds cash value. It allows you to adjust premiums cheaper than traditional whole-life insurance. However, if your investments underperform, your cash value may decrease, and your premiums could increase.

At 210 Financial, we’re here to assist you in finding the policy that fits your family's budget and lifestyle.

Learn More: Debunking the 5 Most Common Misconceptions About Life Insurance

Finding Affordable Healthcare in Retirement:

The game changes when you retire, lose a paycheck, have constant steady work in your life, and your healthcare plan. Now, there are healthcare plans available in retirement for you and your spouse, but you need to look into what plan is going to work best for you both.

Medicare: Diving into all the complex terminology can be overwhelming, especially if you haven't discussed all your potential needs. It's essential to stay informed, so prioritize consulting with a Medicare professional and reading materials that help you better understand the available plans.

- Enrollment: Be aware of the seven-month enrollment window for signing up for Medicare. This period includes three months before your 65th birthday, the month of your birthday, and three months after. You’ll have another opportunity to enroll in the fall, but you may face a financial penalty if you miss the initial enrollment window.

- Applying on Time: It’s essential to apply for your Medicare benefits on time, especially since most retirees rely on it as their primary healthcare plan after leaving the workforce.

- Researching Plans: Medicare offers various plans, and everyone’s health needs are different. It’s important to research each option and consult with a financial professional to determine which plan is best for you.

- Seek Professional Help: Don’t try to navigate Medicare planning and research on your own. Reach out to professionals who can help you understand your options and find the best care for your needs.

- Provider Participation: Keep an eye out for hospitals and healthcare providers that participate in your chosen Medicare plan and offer the services you require.

- Plan: Make sure to plan everything related to Medicare in advance to avoid any complications.

HSA: An HSA, or Health Savings Account, allows you to set aside tax-free money for medical expenses. While it is not exclusively for retirement, it can help cover costs that Medicare or insurance does not cover.

Long-Term Care: Considering a nursing home or any long-term health care that involves significant expenses is an important topic to discuss. Although it may seem distant, delaying this conversation—especially if there is a history of health issues in your family—can be unwise. It’s essential to talk about your options and determine if there are necessary steps you should take together.

Learn More: Planning for the Medical Costs You Don’t See Coming in Retirement

Investment Planning Mindset Shift in Retirement:

Transitioning into retirement resembles a reset, requiring a shift in how you view your finances, daily activities, and investment strategies. Prior to retirement, taking risks can help your money grow and prepare you for this new stage of life. However, once you begin relying on those funds for your living expenses and dreams, your approach must change.

Understanding your risk score and how to manage it for retirement is important. As you age, it’s recommended that you reduce your risk exposure.

To calculate your risk score, use the formula: 100 – your age = your risk score.

The main reason for knowing your risk score is that, while you are young and still earning, you can take on more risk since you have time to recover from any losses. However, as you near retirement, every dollar becomes crucial, and you must lower your risk.

The sequence of returns can significantly impact your retirement savings, especially if you’re forced to sell investments during a market downturn. Once you retire, you will stop contributing to your retirement and will start withdrawing funds instead.

Learn More: Financial Independence Starts with Smart Investing: Are You Taking The Right Risks?

Financial Advisor Specifically for Retirement:

Finding a financial advisor who focuses on retirement planning can help you navigate this new phase of life with someone who understands its complexities. Retirement planning differs significantly from planning during your working years. A retirement advisor can assist you and your spouse in creating a personalized plan that addresses your specific needs.

They can help remove the emotional aspects of planning, develop a comprehensive retirement strategy, and ask essential questions to facilitate important discussions about retirement. Additionally, they can manage your portfolio, allowing you to enjoy this time without financial stress.

Learn More: How a Financial Advisor Can Help You Navigate Retirement Decisions

Legacy Planning for You and Your Spouse:

As a married couple, you have likely accumulated many assets that are worth protecting and passing down in a meaningful way. Creating a legacy plan can help you safeguard the legacy you’ve built through hard work.

To start, list your assets and gather any relevant documentation. Then, consider the following questions:

- Who would you like to leave your property and assets to? Is it one specific person or multiple individuals?

- Are you inclined to support charitable causes? Is there a specific charity you would prefer to give to?

- Do you have any preferences regarding your medical care that should be documented?

After reflecting on these questions and gathering the necessary documents, it's advisable to seek professional assistance. Begin by consulting a financial advisor, and if necessary, consider reaching out to an attorney. A financial advisor can help you develop a comprehensive legacy plan. Having a well-structured legacy plan with all the appropriate legal documents and your wishes clearly outlined can provide you peace of mind and support your loved ones.

Learn More: Leave a Legacy That Matters

Conclusion:

Standing by each other's side through thick and thin is an important commitment filled with love, trust, and hope. As you navigate this next step in your lives together, embrace the fun and excitement it brings. Create a plan to ensure you can both enjoy all the rewards that come with retirement.

Past performance is not indicative of future results. The material above has been provided for informational purposes only and is not intended as legal or investment advice or a recommendation of any particular security or strategy. The investment strategy and themes discussed herein may be unsuitable for investors depending on their specific investment objectives and financial situation. Information obtained from third-party sources is believed to be reliable though its accuracy is not guaranteed, and 210 Wealth Management, Inc., d/b/a 210 Financial makes no representation or warranty as to the accuracy or completeness of the information, which should not be used as the basis of any investment decision. Information contained on third party websites that 210 Financial may link to are not reviewed in their entirety for accuracy and 210 Financial assumes no liability for the information contained on these websites. Opinions expressed in this commentary reflect subjective judgments of the author based on conditions at the time of writing and are subject to change without notice. No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission from 210 Financial. For more information about 210 Wealth Management, Inc., d/b/a 210 Financial, including our Form ADV brochures, please visit https://adviserinfo.sec.gov or contact us at (309)263-1333.

What You Need to Know for Tax Season 2026

The IRS has announced that the 2026 tax filing season begins on Monday, January 26, 2026. Whether you prefer to file your taxes right at the beginning, wait until Tax Day on April 15, or find a balance between the two, it’s essential to complete your filing. Here’s what you need to know about the 2026 tax season in a nutshell. Happy tax filing!

Key Points – What You Need to Know for Tax Season 2026

- One, Big, Beautiful Bill Act:

- Common Retirement Tax Season Questions:

- What to Expect from Tax Season 2026:

- Thinking Beyond This Year's Taxes:

- Conclusion:

A lot has changed regarding taxes since the 2025 season, raising several important questions and issues as we enter 2026. This time of year can be stressful, but it is our responsibility as citizens to pay our dues to support our communities. That being said, let’s avoid becoming the IRS's "customer of the week" by implementing best practices to fulfill obligations while keeping more money in your pockets.

Learn More: Free Tax Explorer Guide

https://210financial.com/guides/

One, Big, Beautiful Bill Act:

Don’t forget about the One Big Beautiful Bill Act that went into effect last year; it could impact your federal taxes this year. Many changes implemented under this act include expanded tax brackets, increased deductions, and new credits designed to maximize refunds for taxpayers.

Overtime pay and tips can significantly improve your financial situation. The new law allows for temporary federal income tax deductions on these earnings, which will be in effect until 2028. Additionally, individuals aged 65 and older can benefit from a new deduction, which permits an extra $6,000 deduction on any income, including taxable Social Security income. It's important to note that some Social Security benefits are taxable, so be sure to double-check your tax obligations.

Tax policies can change with different administrations and other influencing factors, so it’s important to stay informed. This knowledge will help you make the best decisions for yourself and your family.

Learn More: Planning for Taxes in Your Retirement Plan

Common Retirement Tax Season Questions:

Retirement is more than just a lifestyle change; it's a shift in your mindset, and the way you look at taxes changes as well. When determining what you’ll get to keep and what you’ll get to spend in retirement, it may all boil down to taxes.

- Are taxes going up or down in 2026? According to CNBC, the IRS released new income tax brackets for 2026, and with that, the inflation-bashed increased the income ranges for the two lowest tax brackets.

- How do retirement taxes work? In retirement, your income sources change from Social Security to investments and retirement accounts. Instead of receiving a steady paycheck, you will be withdrawing from your savings.

- All About Allocation: Taxes boil down to some questions you have to answer for yourself. Would paying more taxes today mean less over your lifetime? Consider the following illustration and whether your assets primarily reside in qualified (taxed) or non-qualified (not taxed) accounts.

Learn More: IRS Announces First Day of 2026 Filling Season

What to Expect from Tax Season 2026:

Although there are changes this year due to the One Big, Beautiful Bill Act, some aspects of tax season remain the same. This year, tax season starts on January 26th and ends on Tax Day, April 15th. To reduce stress during this time, it's important not to procrastinate on your taxes. Staying organized and ahead of deadlines can help you avoid missing important dates and losing potential deductions.

Keeping accurate and timely records can make the tax season much smoother and more manageable.

- W-2 Forms

- Bank Statements

- Receipts

- Statements From Charities

- Invoices

- Insurance Records

- IRA Statements

- 401(k) Statements

- Other Important Records

It's important to meet with a tax professional or CPA, as they can provide personalized advice and help you navigate the complexities of tax matters. Working with your financial advisor may vary based on the specific tax-related guidance they can offer. However, they can assist you in creating a tax strategy for the current season and for your long-term financial goals, ultimately helping you save on taxes.

Learn More: 6 Retirement Strategies to Consider This Tax Season

Thinking Beyond This Year's Taxes:

Tax planning isn’t just about minimizing what you owe today; it’s about developing a strategy that benefits you in the long term. While tax season comes once a year, having a plan can help you achieve long-term tax efficiency. Tax planning can involve many different elements and varies based on individual needs.

One important aspect to consider is Required Minimum Distributions (RMDs). The IRS mandates that you withdraw money from your pre-tax retirement accounts, such as your Traditional IRA or 401(k), which means you'll incur taxes on those withdrawals. It’s crucial to prepare for this, especially regarding how it might affect future generations. One effective strategy for managing this is a Roth Conversion. This process involves converting funds to a Roth account, which is a post-tax retirement account. You pay the taxes now, while they are lower, which can be a beneficial long-term decision. Shifting your money into a Roth account emphasizes the importance of a well-thought-out tax strategy over simply acting quickly.

Maximizing your contributions to retirement accounts, such as a Traditional or Roth IRA or a 401(k), is another way to save and plan for efficient long-term tax management.

Additionally, legacy planning and taxes are closely linked. A thoughtful approach to legacy planning can help preserve your assets and minimize gift taxes. By creating a legacy plan that focuses on minimizing taxes, you can better navigate the financial implications of the gifts you provide to others, ensuring a more strategic and effective tax strategy.

Learn More: How a Roth Conversion Works (Step-by-Step)

https://www.youtube.com/watch?v=0syWgyWBqwI

Conclusion:

Wishing you a happy and less-stressed tax season. As always, we are here to help guide you and give you the tools and knowledge to succeed this season. Remembering the importance of knowing the tax policies and how they impact you, as well as planning for long-term taxes, and easing through the 2026 tax season.

Past performance is not indicative of future results. The material above has been provided for informational purposes only and is not intended as legal or investment advice or a recommendation of any particular security or strategy. The investment strategy and themes discussed herein may be unsuitable for investors depending on their specific investment objectives and financial situation. Information obtained from third-party sources is believed to be reliable though its accuracy is not guaranteed, and 210 Wealth Management, Inc., d/b/a 210 Financial makes no representation or warranty as to the accuracy or completeness of the information, which should not be used as the basis of any investment decision. Information contained on third party websites that 210 Financial may link to are not reviewed in their entirety for accuracy and 210 Financial assumes no liability for the information contained on these websites. Opinions expressed in this commentary reflect subjective judgments of the author based on conditions at the time of writing and are subject to change without notice. No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission from 210 Financial. For more information about 210 Wealth Management, Inc., d/b/a 210 Financial, including our Form ADV brochures, please visit https://adviserinfo.sec.gov or contact us at (309)263-1333.

If You’re Still Thinking About Retirement Like Your Parents Did, Read This

Change is all around us and can occur slowly over time, like a river carving through rock until a canyon forms, or it can happen as quickly as a lightning strike. Retirement has evolved significantly and will likely continue to change throughout your lifetime, even more so for your grandchildren. In this discussion, we will explore some of the major changes that retirement and retirement planning have undergone. Additionally, we’ll discuss how you can adjust your mindset to embrace a modern approach to retiring.

Key Points – If You’re Still Thinking About Retirement Like Your Parents Did, Read This

- A Shift in Retirement Responsibility:

- Increased Life Expectancy:

- Increased Retirement Age:

- Inflation:

- Conclusion:

- Schedule a Visit

A Shift in Retirement Responsibility:

Your parents or grandparents may have had pensions, which are employer-sponsored retirement plans that provide regular payments during retirement. While some government jobs still offer pensions, most employees are now required to take more responsibility for their retirement savings by using 401(k) plans or IRAs.

401(k) plans offer more flexibility and come with the potential for higher risk and growth, but they also require individuals to manage their investments actively. As the job market has evolved, with fewer people staying at the same job for many years, this flexibility has become increasingly important in navigating the changing landscape of employment.

Increased Life Expectancy:

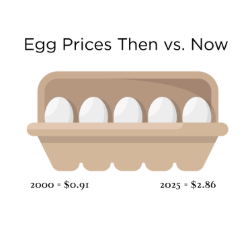

With medical advancements, people are living longer, which leads to longer retirements that need to be financed. Healthcare advancements have significantly contributed to increased life expectancy, but they have also led to rising costs. According to U.S. News, healthcare expenses have surged by over 121% since 2000, even with Medicare coverage.

Living longer is a blessing, as it allows us to witness the growth of our families and the thriving communities we help build. It’s important to be fully engaged in these moments rather than constantly worrying about finances or whether you’ll outlive your retirement savings.

To prepare for those extra years of retirement, it’s essential to consider make a financial plan and understand the risks. Be cautious of the sequence of returns risk, which refers to the potential for poor investment returns occurring early in retirement. When you withdraw from your portfolio during these times, it can damage your investments and leave you vulnerable to running out of money. Timing is crucial in mitigating this risk and ensuring your financial stability throughout a longer retirement.

Learn More: Sequence of Returns Explained (And Why It Matters Most Near Retirement)

https://www.youtube.com/watch?v=5hzWnueMiCQ&t=2s

Increased Retirement Age:

The concept of retirement is evolving; it's no longer just a standard age of 65. Many retirees are choosing to continue working during their retirement years, and there are discussions about potentially increasing the retirement age again.

According to Senior Living data from 2010 to 2019, participation in the labor force among adults aged 65 and older rose from 17.4% to 20.2%. This increase may reflect a desire to stay active or busy, as many older adults feel the need to work. Additionally, the poverty rate among older adults has significantly declined, from 30% in 1966 to 10% today. Improved financial education has played a key role in this reduction.

However, despite the decline in poverty, there are ongoing concerns regarding healthcare costs, rising obesity rates, and chronic conditions. Moreover, issues such as divorce contribute to feelings of loneliness and isolation among retirees.

Learn More: Planning For the Medical Costs You Don’t See Coming in Retirement

Inflation:

Inflation continues to change our perception of money and what a dollar can actually buy. Additionally, older generations have influenced our views on money and retirement. While the impact of inflation is noticeable when purchasing groceries, the more concerning issue is its long-term effects. A 3% annual increase may not seem significant, but it’s important to remember that retirees are living longer than ever, and inflation is a constant factor. It is essential to develop a plan that will help maintain your purchasing power so you can sustain your lifestyle for as long as needed, without financial worry.

Learn More: Are You Aware of Inflation and Its Impact on Your Retirement

Conclusion:

Retirement is set to evolve significantly in the coming years, even more so than it has in the past. What is true for you now may not be the same for your children or grandchildren. Change is a natural part of life and occurs all the time. You can navigate the world of retirement with confidence, and it all begins with a solid plan and the knowledge to help you continue enjoying retirement for many years to come.

GET IN TOUCH

Schedule a Visit

Past performance is not indicative of future results. The material above has been provided for informational purposes only and is not intended as legal or investment advice or a recommendation of any particular security or strategy. The investment strategy and themes discussed herein may be unsuitable for investors depending on their specific investment objectives and financial situation. Information obtained from third-party sources is believed to be reliable though its accuracy is not guaranteed, and 210 Wealth Management, Inc., d/b/a 210 Financial makes no representation or warranty as to the accuracy or completeness of the information, which should not be used as the basis of any investment decision. Information contained on third party websites that 210 Financial may link to are not reviewed in their entirety for accuracy and 210 Financial assumes no liability for the information contained on these websites. Opinions expressed in this commentary reflect subjective judgments of the author based on conditions at the time of writing and are subject to change without notice. No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission from 210 Financial. For more information about 210 Wealth Management, Inc., d/b/a 210 Financial, including our Form ADV brochures, please visit https://adviserinfo.sec.gov or contact us at (309)263-1333.